This note is the first in my series on Manufacturing, Trade, and Jobs, and it focuses on US manufacturing. I present first a historical perspective of US employment in agriculture and manufacturing, and second I look at the contributions of the various industry sectors to the GDP. I find that US manufacturing is stronger now than ever, but the economy has changed and employment opportunities have changed too.

Manufacturing evolution in the national economy

Figure 1 summarizes the evolution of US manufacturing employment. At the birth of the nation, and for many decades afterward, agriculture was the primary activity. In 1800 three-quarters of the labor force was needed to produce food for the nation. Fifty years later agricultural efficiency improved so that only about half of the employed were needed for food production; manufacturing was a significant employer. Throughout much of the 20th-century manufacturers employed between a quarter and a fifth of the workforce; but by 2014 manufacturing employs barely more than 8% of all workers and agriculture and manufacturing together, the total goods-production component of the economy, only employs under 10%. The forecast going forward is for further reductions in the fraction of the labor force producing goods.

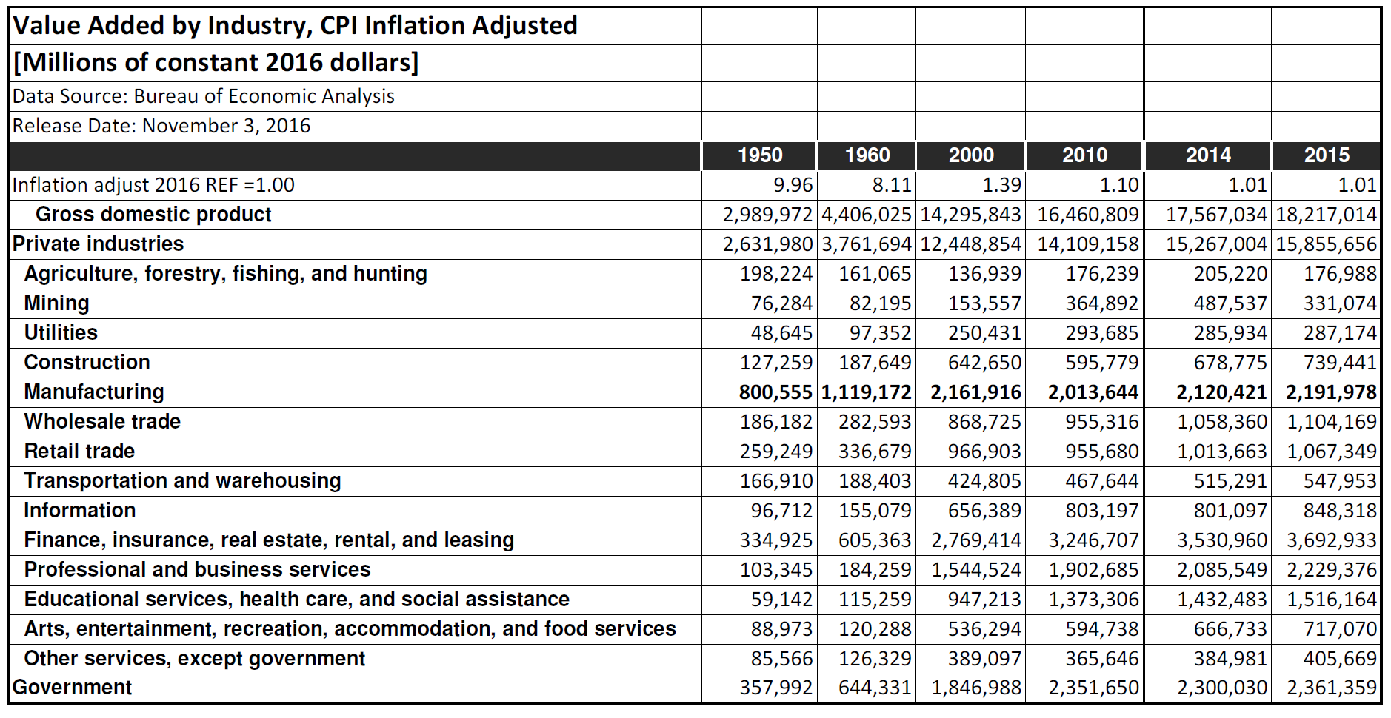

So, what happened; did manufacturing die? Not at all. As Figure 2 shows, in constant inflation-adjusted dollars, the value added by manufacturing to the national economy grew steadily in the second half of the 20th Century from $0.8 Trillion in 1950 to over $2.1 trillion in 2014.

Figure 1

What happened is that as production efficiencies improved fewer people were needed to produce goods. In 1950 about 16 million workers produced $0.8 Trillion worth of manufactured goods, at a productivity of $50 thousand/head; in 2014 about 12 million workers produced more than $2.1 Trillion at a productivity of $174 thousand/worker (again in constant inflation-adjusted $ values, based on data from Figures 1 and 2).

Figure 2

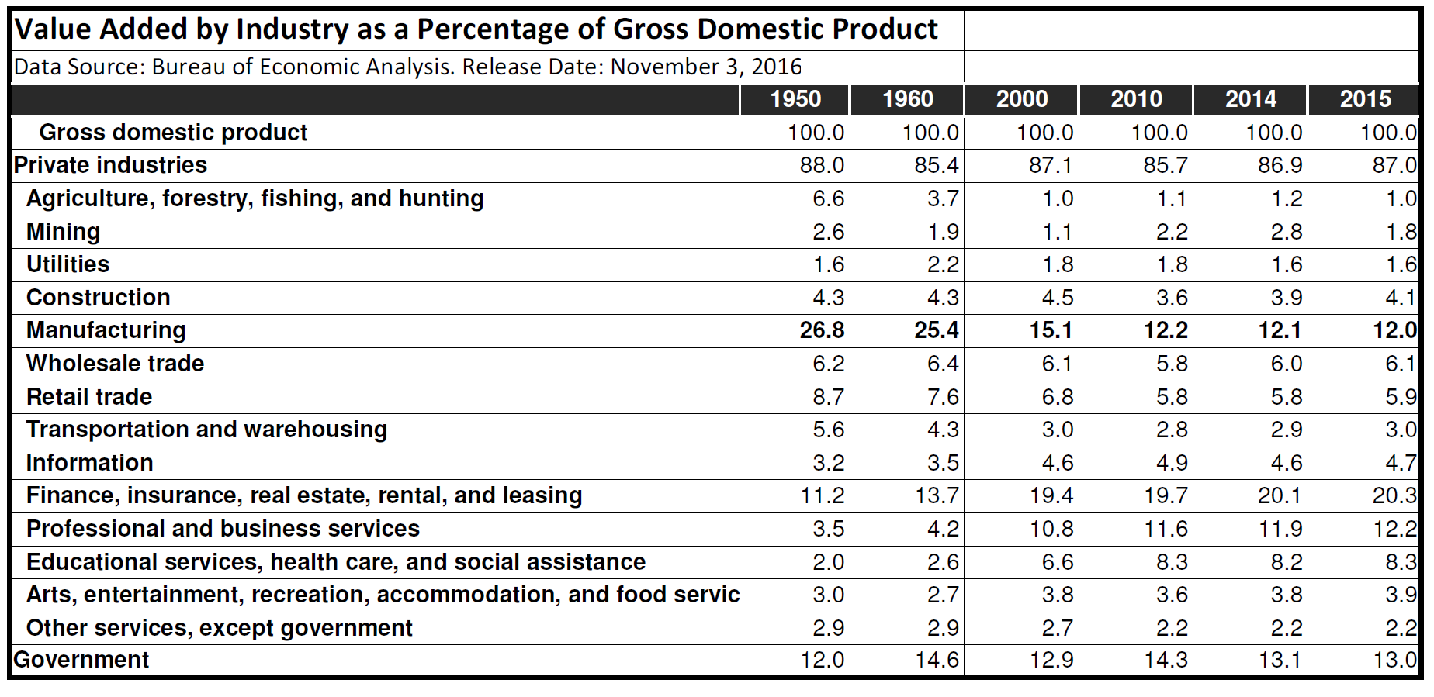

Figure 3

Furthermore, as the economy grew, even though the value added by manufacturing to the national economy grew, the percentage contribution of manufacturing steadily decreased. Figure 3 shows the value added as a percentage of the GDP. Manufacturing’s fractional contribution decreased from about 27% in 1950 to about 12% in 2014; even though the value created by it grew more than two-and-a-half-fold. The economy grew even faster, close to six-fold over the same period. Also, as shown in Figure 1, during this period the population about doubled, thus the per head value of manufactured goods in constant dollar terms grew faster than the population, from about $5-thousand/head in 1950 to close to $7-thousand/head. Furthermore, due to technology advances, the features (and user benefits) of manufactured goods per constant dollar purchase price greatly improved.

Times change and old industries get replaced

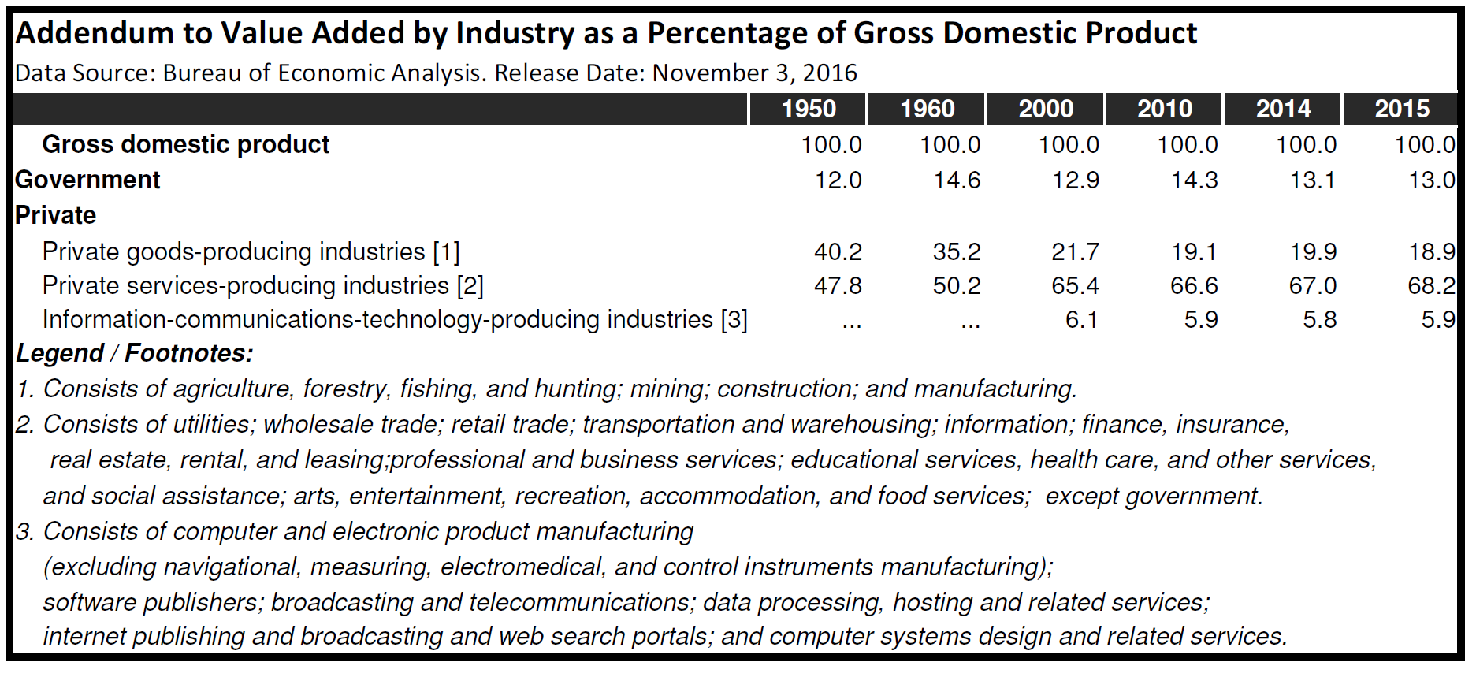

As the economy has been growing the various industry segments have grown at different rates. As is well known, in about 200 years the US economy morphed from an agricultural origin through a heavily manufacturing-oriented phase to a service economy. Figure 4 presents a summary view of this transition. The trend from goods production activities to services is obvious, and this trend is likely to continue.

Conclusion

From the foregoing, we conclude that US manufacturing is stronger than ever and continues to thrive. But the composition of the economy has changed, with services having assumed the dominant role. In recent years (beginning in 2000), the US Bureau of Economic Analysis shows Information-Communications as a separate line item, indicating the growing significance of this relatively new industry in the continuously evolving economy. Also, the structure of manufacturing has changed: today fewer people produce two-and-a-half times more value than more people produced 60 years ago. This secular trend of productivity improvement continues, inevitably leading to job losses, unless growth in demand exceeds growth in productivity and/or US-produced goods

Figure 4

provide superior cost-performance benefits to that offered by foreign manufacturers. Not likely scenarios, thus I expect that US manufacturing will continue to grow in absolute dollar terms, but its share of the GDP will shrink, and its share in US employment will continue to shrink too. In fact, not only manufacturing’s percentage share of the employed will continue to shrink, but so will the total number of people employed in the manufacturing sector of the growing US economy supporting a growing US population. - - No amount of populist haranguing and no endless stream of misguided presidential initiatives will change these long-term trends.

.

No comments:

Post a Comment